Economies at War: Revisiting the Palestine-Israel Conflict

Abhinish Boora and Chhandashree

Overview

The origins of the Israel-Palestine conflict can be traced back to the late 1800s, when the Zionist movement emerged. Since then, over the last century and a half, the conflict has gone through several phases, notably influenced by the two World Wars, Nazi pogroms, the decline of the British Empire, and the rise of new geopolitical dynamics. In response to these complex historical developments, the United Nations General Assembly proposed partitioning Palestine into Arab and Jewish states in 1948. However, this proposal did not result in a resolution; instead, it precipitated a protracted Israel-Palestine civil war that has yet to be resolved.

This paper aims to examine the economic dimensions of the protracted conflict, an aspect that has received inadequate attention due to an overwhelming focus on its political facets. The comprehensive understanding of the conflict has been impeded by the persistence of an unjustifiably favoured and unilaterally dominant perspective. In addition to this, the underemphasized roles of various forms of sanctions imposed on the parties under scrutiny have also been investigated. This inquiry seeks to uncover the impact of the sanctions on the current scenarios, thereby contributing to a more nuanced understanding of the conflict.

To meet the objective of the paper that is to unveil the consequences of the sanctions on the Israeli and Palestinian economy as well as to understand or analyse the effect of those consequences of the sanctions on the current economy, we have made use of the following databases: The Threat and Imposition of Sanctions (TIES) database, to make a list of the sanctions that the United States and the former Soviet Union have put on Arab countries and Israel; The United Nations Conference on Trade and Development (UNCTAD) database, to get economic and demographic data for Palestine; and The International Monetary Fund (IMF) database, which provides GDP and inflation trends for Israel and Palestine from 1980 to 2023.

The economic contrast

The International Monetary Fund (IMF) projects that Israel’s GDP would reach $522 billion in 2023. In contrast, the World Bank estimates that the total GDP of Palestine will be less than $20 billion, a difference of over 26 times. Notably, compared to Israel’s $51,800 GDP per capita in 2021, Palestine had a meagre $3,460 per year. This enormous economic gap highlights both a considerable wealth gap and a continued lack of significant rise in Palestinian income levels relative to Israel’s consistently prosperous state.

Despite the apparent economic disparities between Israel and Palestine, a more detailed examination of economic performance metrics highlights the interconnectedness of both economies.

Source: Economy and statistics | UNCTAD, Israel Inflation Rate 1960-2023 | MacroTrends

Fig:1

According to the United Nations Conference on Trade and Development (UNCTAD), approximately one-fifth of the labor force in the West Bank is employed by Israel. This significant cross-border employment contributes substantially to the striking similarity in inflation rates between Israel and Palestine. This mutual dependence prompts a crucial question: despite Israel’s robust economic growth, why does the Palestinian economy, closely tied to Israel, persist in experiencing stagnation?

Fig: 2

Source: Economy and statistics | UNCTAD, Israel Inflation Rate 1960-2023 | MacroTrends

Fig :3

In Palestine’s situation, constrictive circumstances impede the fundamental requirements for economic expansion. In particular, the Gaza Strip has long served as a containment zone, with no official commerce routes and a preponderance of reliance on international charity and the UN for financial support. Economic advancement is obstructed by the lack of trade links with other countries and increased political instability, which reduces the probability of foreign investments. In addition, Israel has an impact on the Palestinian human resource, which is similar to the region’s economic enslavement. The map (Fig:4) illustrates the sole three crossing points that permit access to and from the Gaza Strip, a region subjected to stringent restrictions:

Information: OCHA, Humanitarian Data Exchange

Fig:4

1946-1964: Birth and growth of Israel

The 1947 UN Partition Plan for Palestine divided Palestine into Arab, Jewish, and Special International Regimes, sparking a civil war. The US supported the resolution, leading to Arab armies attacking former Palestinian land. Israel was established in 1948, with US President Truman acknowledging the Balfour Declaration.1

The British opposed a Jewish and Arab state in Palestine due to their commercial dominance in the Ottoman Empire’s Levant and the Suez Canal. The US supported Resolution 1812, but the State Department proposed UN trusteeship with Jewish immigration limits and division of Palestine.In 1949, Israel signed Armistice Agreements with Egypt, Lebanon, Jordan, and Syria, ending the 1948 Arab-Israeli War and establishing the Green Line. Israel acquired Palestinian territories, leading to the Suez Crisis in 1956 and the exile of the Palestinian Authority. In 1959, Egypt absorbed the All-Palestine Government, resulting in military control of Gaza. In 1967, Israel captured Palestine, including East

Jerusalem. Palestinian demands ranged from dissolution to self-determination.

The US and USSR aimed to maintain power balance in the Middle East by imposing sanctions on target nations and Israel to maintain control and counter Arab nations’ desire to dismantle the idea of an independent Jewish State, despite not actively participating in armistice discussions.

Sanctions, treaties and agreements with US and USSR

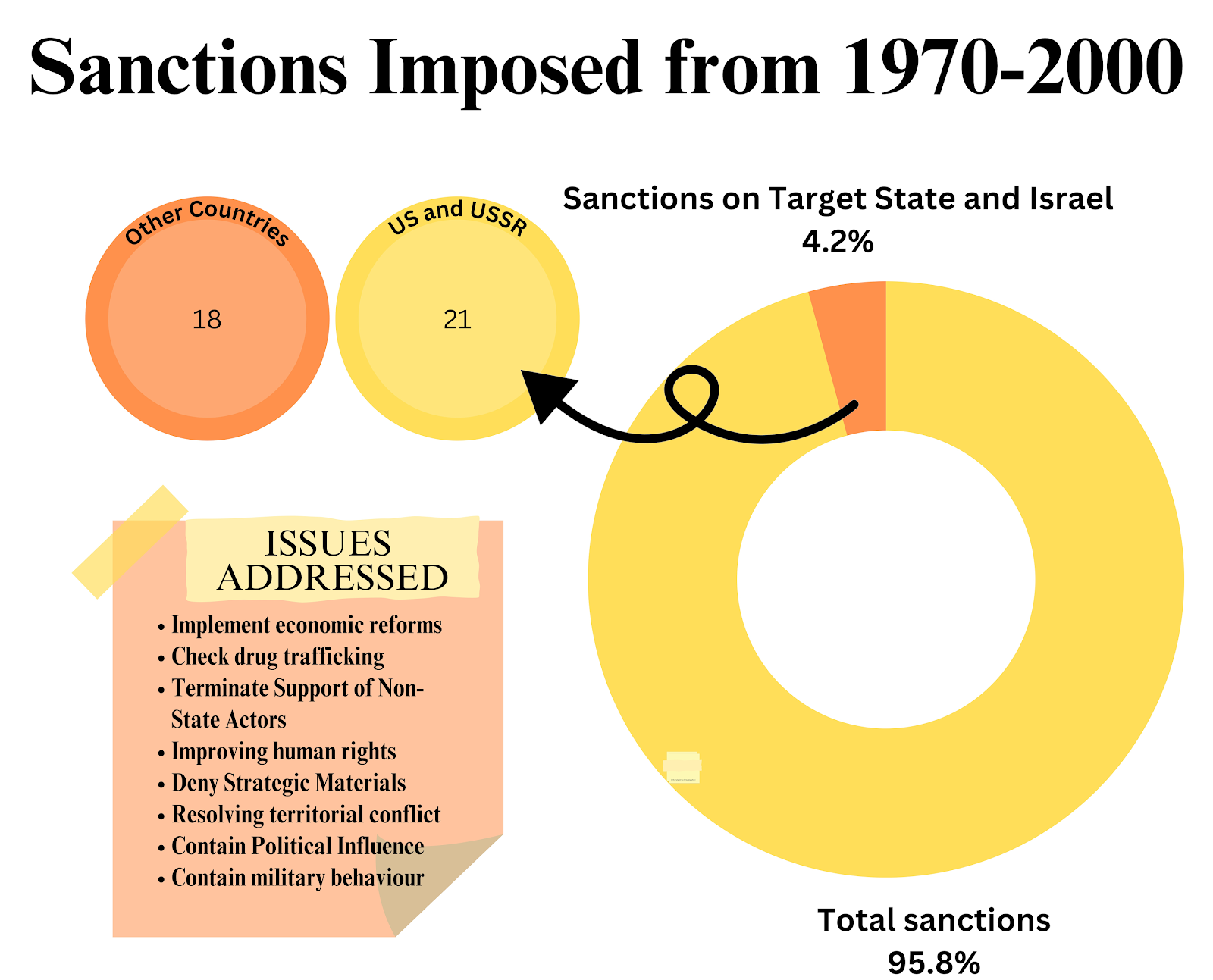

Following prolonged conflicts between Arab nations and Israel, a series of sanctions, treaties, and agreements were established to maintain peace and cooperation. Global powers like the US and the former Soviet Union (present-day Russia) played a pivotal role in implementing sanctions against nations that posed threats or engaged in unjust economic or political practices. Out of 39 sanctions imposed, 21 were jointly imposed by the US and USSR.

The following information about the sanctions is being acquired from TIES (Threat and Imposition of Economic Sanctions). The database provides details about all the sanctions that have been imposed by different countries on others. It consists of all the information about the sanctions imposed, such as the sender(states that either initiate threats against target states or impose sanctions against the target state), target states(the nations on which the sanctions are imposed), identity (identifies the part of the sender that is responsible for the imposition of sanctions, ex- government or Judicial etc.), the issue for which it is imposed(capture as best as possible the issue(s) involved in the imposition of sanctions), sanction type threatened (captures the threat posed by the sanctions or categories of sanctions types threatened by the sender), sanction type (captures the type of sanctions imposed), settlement nature of target as well as sender states (to what extent the sanctions benefitted).

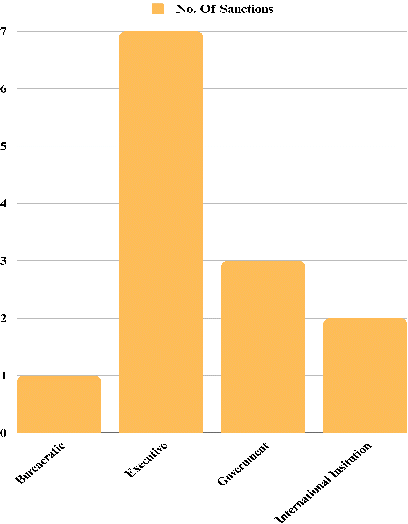

From the 1970s to the 1990s, the US and USSR placed 13 sanctions on selected governments, including Israel. Five of these penalties were imposed by the executive branch, and they included the suspension of foreign aid, limits on export activity, and partial economic embargos. Two were government employees and one was a bureaucratic body with varied degrees of impact and strength. Eight sanctions were imposed after 1990, including two from the executive branch, one from the government, and one from an international entity such as the UN.

The visual illustration (Fig:5) explains where the penalties came from to the target states till date. It can be seen that most of the impositions came from the executive body addressing the issue of increased military activities, target states extending support to any terrorist organisation, economic policy reforms, trade practices adopted etc. Those imposed from the government side were imposed for addressing a much broader issue which involves political aspects, such as the alliance of the target state with a third party (can be another nation or terrorist organisations) and territorial dispute etc.

Fig:5

From the 1970s to the 1980s, two sanctions were applied specifically to Egypt and Libya, addressing the issue of third-party alliances with the target states. Export restrictions were instituted, limiting the supply of certain commodities from the US to Egypt. Additionally, previous economic agreements with the target states (Egypt, Syria, Lebanon, Libya, Saudi Arabia, and Iraq) were either annulled or terminated. The sanctions aimed to address the escalating tensions and reduce the likelihood of further conflicts between Arab and Jewish states.

Since the 1970s, peace efforts have been made in the Arab-Israeli and Palestinian-Israeli conflicts, with some nations signing treaties and others remaining unresolved. US officials and lobbying groups have different perspectives.

In the 1980s and 1990s, the US imposed 11 sanctions, four of which targeted Israel to correct disproportionate military activities and resolve issues between target states and Israel. These sanctions resulted in import and export restrictions for Israel. Four sanctions were imposed on Iraq and Egypt to address concerns about excessive military actions, military capabilities, human rights advancement, and economic reform. These sanctions restricted military supply through a partial economic embargo and required foreign aid suspension or threat,subject to compliance with US directions.

Fig: 6

Between 1990 and 2000, the United States imposed eight sanctions, primarily targeting Arab nations, primarily Arab League member states. These sanctions were aimed at increasing non-military influence, military operations, military acquisitions, alliance formation, and support for transnational terrorist organizations. They could lead to an economic embargo, halting commercial transactions, and limiting military supply. Additionally, they could result in a blockade, barring other governments from participating in economic transactions with the target state. The sanctions were often enacted in coordination with foreign organizations, such as the United Nations.

From the TIES data of sanctions for the period of 1970-2000, it was found that out of 21 sanctions imposed on the Arab League along with Israel by the US and USSR, 12 of those settlement nature is known. The average settlement nature of the target states was found to be 2.9 ranging from 0-7 whereas the average settlement of the sender state (US and USSR) was 4.5 ranging from 0-9. This indicates that the sanctions imposed favoured the sender states.

The figure below (Fig:8) shows the different types of sanctions that have been imposed and their frequencies. It can be seen that the major sanctions were on putting restrictions on exports from target states. This is a major take that gives a clear idea about the probable effects. Majorly, the slowdown of the economy, hindrances in forming international relations etc.

Fig:7

Fig:8

The aforementioned sanctions, with the primary weight borne by the targeted states, imply a substantial impact that is evident in the current scenarios discussed in the ‘Economic Contrast’ section. This is indicative of the ongoing significant consequences generated by these sanctions, particularly in illuminating the economic disparities between the two studied economies.

Impact on the Global Economy

Crude oil prices have long been susceptible to political instability in the Middle East, an area with the most oil riches in the world.

Yet, the current war between Israel and Hamas has had little influence on global commodities markets. Oil Israeli-Hamas conflict, whereas most industrial metals, agricultural commodities, and other commodities have seen little to no price swings. Conflict in the Middle East may send shockwaves throughout the world since the region is a vital supply of oil and a vital shipping route. The best example is the Arab-Israeli conflict of 1973, which resulted in an oil embargo and years of stagflation in industrial economies.

The above-mentioned information and the following representation (Fig:9) have been taken from Bloomberg. It deals with various aspects including economics which offers a comprehensive macroeconomic research service for Bloomberg Terminal subscribers. That includes rigorous, original thematic research, supporting detailed economic forecasts. The economists also produce previews of major data releases or economic events and analysis as the key numbers break.

Bloomberg, a privately held financial, software, data, and media corporation, has purchased RegTek—solutions to broaden its regulatory reporting and data management offerings. According to Bloomberg, the agreement combines the experience of both companies to develop a holistic solution that combines data enrichment and reporting capabilities with RegTek.Solution’s quality and control tools across many reporting jurisdictions.

Source: Bloomberg

Fig:9

As per the report of The Economics Times, rising oil prices reaching $90 would have an impact on the global economy. Further escalation of the conflict towards other Middle Eastern oil producers is dangerous and must be closely monitored, particularly given the global economy’s ‘higher for longer’ interest rate scenario. The oil supply is unlikely to be jeopardised unless the dispute spreads to other countries in the area and turns into a proxy fight between the US and Iran.

Any reprisal against Tehran might jeopardise ships transiting the Strait of Hormuz, which Iran has threatened to restrict. This will boost global shipping and insurance costs, as well as already rising oil prices. Brent had surpassed the $90 barrier before retreating. We may now use the $90 figure to denote the point at which the global economy is in jeopardy. As crude oil prices climb, the global economy will confront severe inflation once more. If oil prices remain high, the United States, India, China, and other large oil-importing countries may face significant import inflation.

When oil prices rise, the cost of production for numerous industries as well as energy expenses for businesses and consumers rise, causing inflation to rise. High energy costs and new inflationary tendencies might weaken central banks’ attempts to control inflation.

Fig:10

In this scenario, the global economic effect is caused by two shocks: a 10% increase in oil prices and a risk-off move in financial markets similar to what occurred during the Arab Spring.

They add up to a 0.3 percentage point drag on global GDP next year, or around $300 billion in lost production, slowing the rate to 2.4%. Except for the 2020 Covid crisis and the global recession of 2009, that would be the slowest growth in three decades.

Higher oil prices would also contribute approximately 0.2 percentage points to global inflation, keeping it close to 6% and putting pressure on central bankers to maintain restrictive monetary policy even if GDP disappoints.

Source: Bloomberg

Fig:11

Conclusion:

There are two primary takeaways that are pointed out in the paper. 1) Arab Nations and sanctions: In order to keep a check on the rising dispute over land and economic differences the global powers US and USSR imposed certain sanctions/penalties on targeted Arab nations. Another motive behind imposing the sanctions was to keep the hold of the power and not let it slide to other global powers. The imposition of the sanctions brought with it very obvious circumstances which affected the economic situation as well; 2) Impact on the Economy and UN: The elongated conflict turned war has had notable economic consequences both for the domestic country as well as globally. The Arab Nations are the largest producers of oil and hence the tension in the area pushes the prices and the inflation rate upward, tightening the global economy. Despite of visible economic harm which is felt globally, the war is majorly highlighted as a humanitarian truce by the UN, ignoring the possible and very likely economic stress. UN called for an Emergency Session to discuss the ongoing war (Israel-Hamas War 2023) and focused on providing humanitarian aid to the victims of the stressed areas. But not much of an attention is diverted towards the economic agenda. The economic consequences are particularly remarkable and worrying, as their impacts are likely to last long after the conflict is over. This may entail changes to multiple laws and reforms, eventually hindering national growth and development.

For further Reference

- Balfour Declaration

- British Mandate

- A humanitarian truce is recognized as a ceasefire between fighting parties so that civilians who are exposed to violence and the impacts of war can get access to much-needed aid.

- The Suez Crisis 1956

“The Suez Crisis, or the Second Arab–Israeli war, also called the Tripartite Aggression in the Arab world and the Sinai War in Israel, was an invasion of Egypt and the Gaza Strip in late 1956 by Israel, followed by the United Kingdom and France. The aims were to regain control of the Suez Canal for the Western powers and to remove Egyptian president Gamal Abdel Nasser, who had just[13] nationalised the foreign-owned Suez Canal Company, which administered the canal. Israel’s primary objective was to re-open the blocked Straits of Tiran. The Suez Canal was closed from October 1956 until March 1957. Israel fulfilled some of its objectives, such as attaining freedom of navigation through the Straits of Tiran, which Egypt had blocked to Israeli shipping since 1948–1950.”

- Why Israel- Hamas War?

- Why fight over the Gaza Strip?

- Why is the Suez Canal important? And what led to the Suez Crisis?

- Brief of Israel- Palestine conflict till now

- Arab- League

- Economy of Palestine

- UN takeaway- Israel & Palestine

References:

- Britannica, T. Editors of Encyclopaedia (2023, October 26). Balfour Declaration. Encyclopedia Britannica. https://www.britannica.com/event/Balfour-Declaration

- “British Colonialism, Middle East .” Encyclopedia of Western Colonialism since 1450. . Retrieved October 18, 2023 from Encyclopedia.com: https://www.encyclopedia.com/history/encyclopedias-almanacs-transcripts-and-maps/british-colonialism-middle-east

- Sicherman, H. , Elath, . Eliahu , Ochsenwald, . William L. and Stone, . Russell A. (2023, November 6). Israel. Encyclopedia Britannica. https://www.britannica.com/place/Israel

- Britannica, T. Editors of Encyclopaedia (2023, October 17). Palestine Liberation Organization. Encyclopedia Britannica. https://www.britannica.com/topic/Palestine-Liberation-Organization

- Britannica, T. Editors of Encyclopaedia (2023, November 6). Gaza Strip. Encyclopedia Britannica. https://www.britannica.com/place/Gaza-Strip

- https://www.reuters.com/world/middle-east/whats-israel-palestinian-conflict-about-how-did-it-start-2023-10-30/

- TIES Data Page Threat and Imposition of Sanctions (TIES) Data Page (unc.edu)

- Palestine: Economy and Statistics (UNCTAD) Economy and statistics | UNCTAD

- Israel Economy (IMF) IMF Data

- Udit Misra: Comparison between the economies of Palestine and Israel ExplainSpeaking: Comparison between the economies of Palestine and Israel in 6 charts (indianexpress.com)

Authors are Post Graduate students of Economics at the Dr B R Ambedkar School of Economics University, Bengaluru.

Correspondence Email: Chhandashree (222PGF008@base.ac.in) and Abhinish Boora (222PGF002@base.ac.in)

Disclaimer: The views and opinions expressed in the blog posts on this website are solely those of the individual authors and do not necessarily reflect the official policy or position of Dr. B. R. Ambedkar School of Economics University. The authors are responsible for the accuracy and completeness of the information presented in their blog posts. The University does not endorse or guarantee the accuracy, completeness, or timeliness of any information provided in these blog posts.